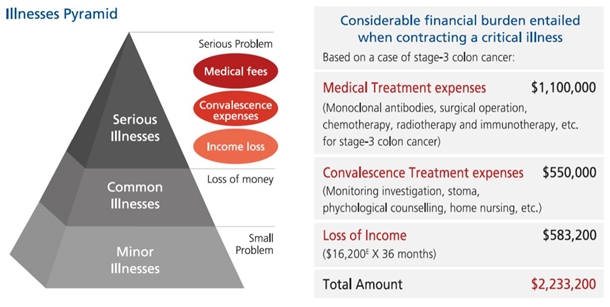

When a critical illness strikes, not only will you lose your health, but also your wealth.

Remarks: The above treatment expenses are hypothetical, are provided by a registered medical specialist, and are for reference only. Actual fees depend upon the actual medical condition, medication, fees charged by attending doctors and hospitals, etc. The income amount is based on the median monthly wage of employees in the 2016 Report on Annual Earnings and Hours Survey, Census and Statistics Department, Hong Kong (Published in March 2017).

Source:

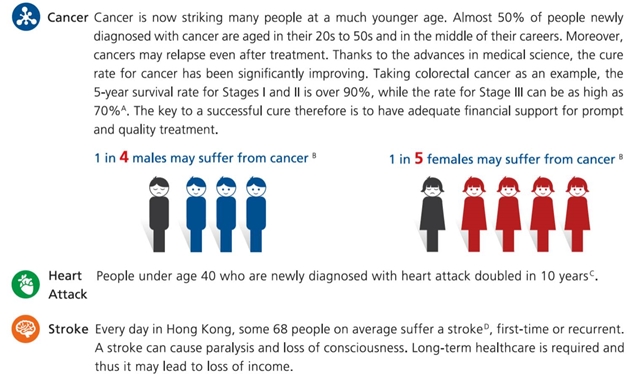

A Figure(s) collected from the website of CUHK Jockey Club Bowel Cancer Education Centre (downloaded in December 2017).

B Percentage of Hong Kong people developing cancer before the age of 75, according to 2014 Hong Kong Cancer Statistics, Hong

Kong Cancer Registry, Hospital Authority, Hong Kong (published in November 2016).

C Information from Hospital Authority, Hong Kong (2010).

D Statistical Report, Hospital Authority, Hong Kong (Published in May 2016).

E The income amount is based on the median monthly wage of employees in the 2016 Report on Annual Earnings and Hours Survey, Census and Statistics Department, Hong Kong (Published in March 2017).

MassMutual Asia’s PrimeHealth Saver 1000 is an insurance solution that bundles critical illness, life protection and savings into one single policy. The plan allows multiple claims for common critical illnesses, such as Cancer, Heart Attack and Stroke. It also offers Benign Extra Care. This is no doubt the prime choice for safeguarding your health.

You can enjoy absolute peace of mind, knowing that the benefit term of the plan may last up to age 100. You may also select from three premium-payment term options: 10 Years, 15 Years and 20 Years to best suit your needs. Best of all, beyond the premium-payment term, you will continue to enjoy full protection without paying any further premiums.

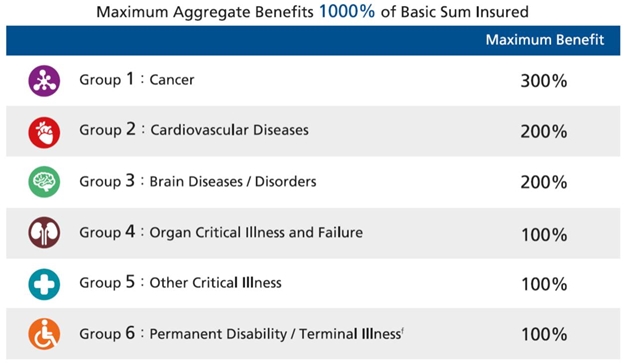

1000% Extensive Coverage

1000% Extensive Coverage

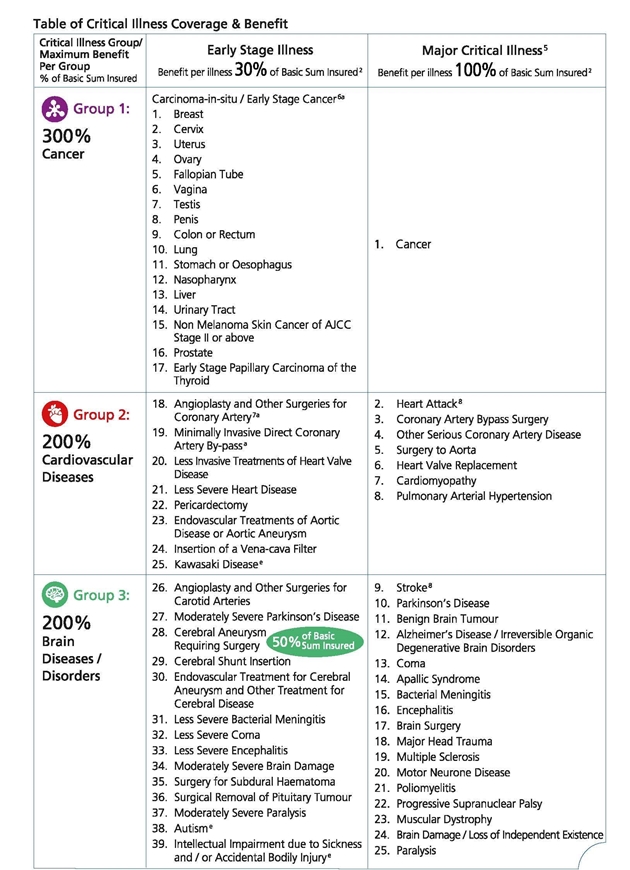

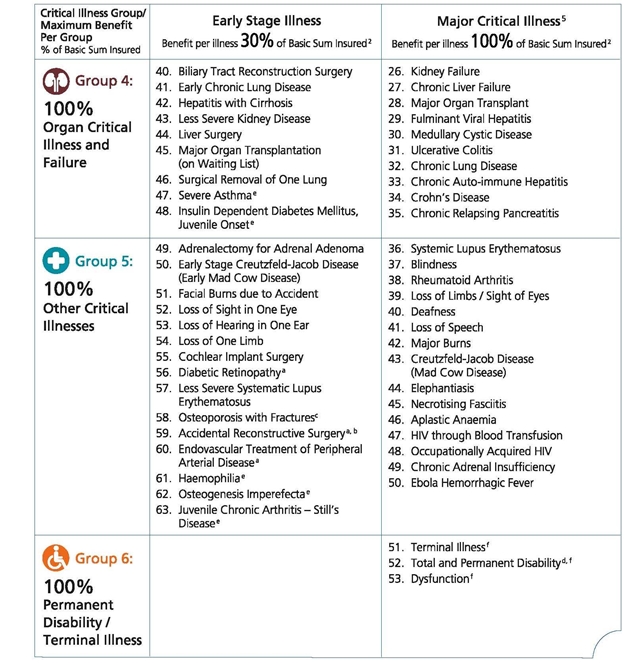

PrimeHealth Saver 1000 covers up to 116 Critical Illnesses, i.e., 53 “Major Critical Illnesses” and 63 “Early Stage Illnesses”, including various Carcinoma-in-situ/Early Stage Cancers and Severe Child Diseases. All Critical Illnesses are categorized into 6 Critical Illness Groups. Each Group offers an individual maximum benefit, with the maximum aggregate benefits of all Groups up to 1000% of the Basic Sum Insured1. The benefits are provided in two phases as shown below.

Phase 1: 100% of Basic Sum Insured

This phase provides a total benefit2 of 100% of the Basic Sum Insured plus “Extra Bonus3” and "Terminal Bonus3", with coverage of 116 "Early Stage Illnesses" and "Major Critical Illnesses", up to age 100.

Phase 2: 900% of Basic Sum Insured

After the total benefit paid has reached 100% of the Basic Sum Insured4, no further premiums are required. The policy will remain in force and continue to provide the Insured with "Major Critical Illnesses"5 coverage of up to 900% of the Basic Sum Insured during Phase 2, which may last up to age 75.

Remark: The above example is based on a male, non-smoker, and a 20-year premium payment term. It is for illustrative purpose only. Please refer to the policy document for benefit coverage and exact terms and conditions.

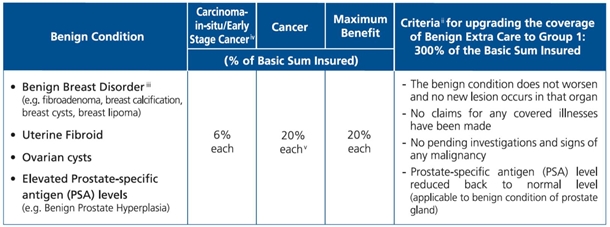

Benign Extra Care

Benign Extra Care When taking out an insurance application, if the Insured has already been diagnosed with the below benign conditions, cancers developed from the corresponding organ will usually be regarded as an exclusion.

However, PrimeHealth Saver 1000 will offer Benign Extra Care with total benefits payable up to 20% of the Basic Sum Insuredi for cancers developed from the corresponding organ diagnosed with benign conditionsi, provided that the underwriting requirements are met.

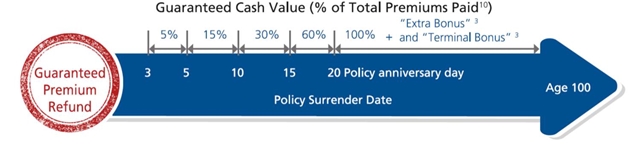

From the 2nd to 6th Policy Yearii, the Insured may submit the required documents to us to upgrade the coverage of the Benign Extra Care to 300% of the Basic Sum Insured originally provided in Group 1 of this plan, provided that the underwriting requirements are met. Guaranteed Refund of Premiums - In Phase 1, if you surrender the policy at the 20th policy anniversary or onwards, the plan offers you a guaranteed "Refund of Premiums"10, an “Extra Bonus” 3 and a "Terminal Bonus"3, without deduction of any claims paid2. What's more, starting from the 3rd policy anniversary onwards, the plan offers you a partial "Refund of Premiums" upon policy surrender.

i. Applicable only to cancers covered under the “Benign Extra Care” as specified in the Endorsement. The insured must survive for at least 14 days from the date of diagnosis of a Critical Illness. The coverage of Benign Extra Care may last up to age 75 of the Insured or when the coverage of Phase 1 ceases, whichever is later.

ii. Subject to the applicable underwriting rules at the time of application.

iii. The Insured with any breast reconstruction surgery (e.g. breast augmentation) performed before/after taking out the policy is not qualified for Benign Extra Care/upgrading the coverage of Benign Extra Care.

iv. Subject to US$50,000 / HK$/MOP400,000 per life limit under all benefits issued by the Company.

v. Net of any Carcinoma-in-situ/Early Stage Cancer benefits paid under Benign Extra Care for the same organ.

a Subject to US$50,000 / HK$/MOP400,000 per type of illness per life limit under all benefits issued by the Company.

b Reimburses the actual amount of hospitalization and medical expenses not yet reimbursed.

c Subject to US$50,000 / HK$/MOP400,000 per type of illness per life limit under all benefits issued by the Company; coverage may be provided up to age 70 of the Insured.

d Coverage for “Total and Permanent Disability” is only applicable to Insured aged 18-65.

e All Severe Child Diseases in total may be claimed once only, and the coverage may last up to age 25 of the Insured, subject to US$50,000 / HK$/MOP400,000 per life limit under all benefits issued by the Company.

f Coverage for Terminal Illness, Total and Permanent Disability and Dysfunction is only applicable to Phase 1 when the total benefit paid has not reached 100% of the Basic Sum Insured4.

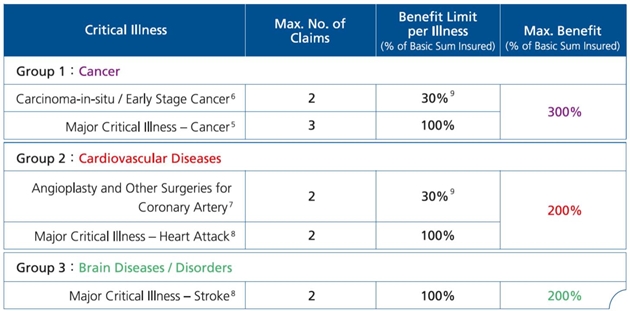

Extra Claims

Extra Claims

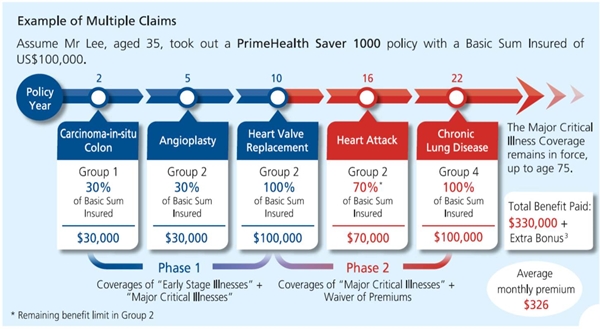

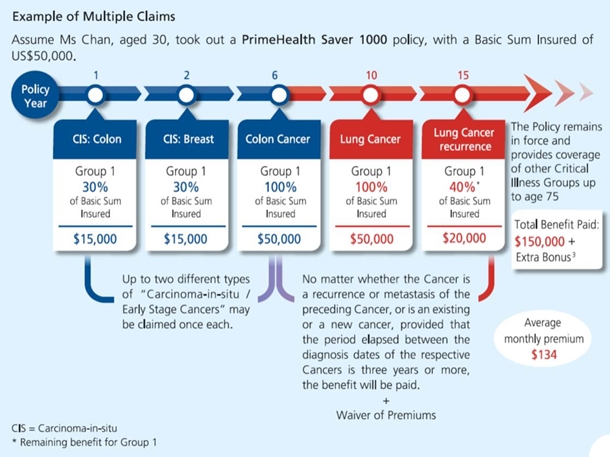

PrimeHealth Saver 1000 provides multiple claims for critical illnesses with a higher rate of recurrence, including Cancer, Heart Attack and Stroke:

Remark: The above example is based on a female, non-smoker, and a 20-year premium payment term. It is for illustrative purpose only. Please refer to the policy document for benefit coverage and exact terms and conditions.

Extra Guarantees

Extra Guarantees

Guaranteed Refund of Premiums - In Phase 1, if you surrender the policy at the 20th policy anniversary or onwards, the plan offers you a guaranteed "Refund of Premiums"10, an “Extra Bonus” 3 and a "Terminal Bonus"3, without deduction of any claims paid2. What's more, starting from the 3rd policy anniversary onwards, the plan offers you a partial "Refund of Premiums" upon policy surrender.

Guaranteed Waiver of Premiums - After the total benefit paid has reached 100% of the Basic Sum Insured4, not only will you continue to enjoy the Phase 2 coverage of "Major Critical Illnesses" with total benefit up to 900% of the Basic Sum Insured up to age 75, but also a waiver of premiums for the remaining premium-payment term while the policy remains in force.

Dual Bonuses

Dual Bonuses

During Phase 1, you will enjoy:

Extra Bonus - An Extra Bonus3 will be credited to your policy on the 5th policy anniversary and every 5 years thereafter. You may withdraw the Extra Bonus at your total discretion, or accumulate it in your policy account for higher returns.

Terminal Bonus - From the 20th policy anniversary onwards, the “Terminal Bonus” will be declared annually for the following twelve-month period and will be payable upon the maturity or surrender of the policy, or upon the death of the Insured or the total benefit payments being 100% of the Basic Sum Insured4.

Extra Life Protections

Extra Life Protections

Life Protection - In the unfortunate event of the death of the Insured during Phase 1, the life protection benefit2 will be paid to the beneficiary.

Extension of Life Protection - We understand that, in the unfortunate event of being diagnosed with a critical illness, one may like to give extra protection to the family. Therefore, without the need to provide any satisfactory proof of insurability, the Insured may opt to take out a permanent life insurance plan within 90 days11 following the end of one year after diagnosis of a Critical Illness with the total benefit paid reaching 100% of the Basic Sum Insured4. The sum insured of the life insurance plan may be up to 100% of the Basic Sum Insured under the plan.

MediNet Pro

MediNet Pro

Currently, more than 4,000 US hospitals are members of the MediNet Pro network. If the Insured has been diagnosed with any of the covered illnesses, the following services are available:

1) second medical opinion provided by US medical specialists12, and

2) quality treatment referrals in the USA12 - the Insured may receive quality treatment at a discounted price.

Remark: For the definition of each "Major Critical Illness","Early Stage Disease", “Carcinoma-in-situ / Early Stage Cancer", and "Severe Child Disease", please refer to the policy document.

Notes

1 If more than one Critical Illness diagnosed on the same day are arising from the same illness or injury, the claim will be paid once only for the Critical Illness with the higher benefit amount.

2 Net of policy debt (if any).

3 “Extra Bonus” and "Terminal Bonus" are not guaranteed.

4 Not including benefit paid under Benign Extra Care.

5 Conditions for the coverage of "Major Critical Illnesses" in Phase 2:

(a) the Insured must survive for at least 14 days from the date of diagnosis of a Major Critical Illness; and

(b) the period elapsed between the diagnosis dates of a Major Critical Illness and the immediate preceding Major Critical Illness must be at least one year, and:

i) if the Insured has received Major Critical Illness benefit for Cancer and is subsequently diagnosed with Cancer again, no matter whether the Cancer is a recurrence or metastasis of the preceding Cancer, or is an existing or a new Cancer, the period elapsed between the diagnosis dates of the respective Cancers must be at least three years;

ii) if the Insured has received Major Critical Illness benefit for Cancer and is subsequently diagnosed with "Group 4: Organ Critical Illness and Failure", the period elapsed between the two diagnosis dates must be at least five years;

iii) if the immediate preceding Major Critical Illness claim is for “Group 6: Permanent Disability / Terminal Illness”, the period elapsed between the two diagnosis dates of the subsequent Major Critical Illness and the above illnesses must be at least five years; and

(c) coverage is not applicable to “Group 6: Permanent Disability / Terminal Illness”

6 Benefits for up to two different types of "Carcinoma-in-situ/Early Stage Cancer" may be claimed once each.

7 To be eligible for a claim, the coronary artery must have stenosis of 50% or higher; to be eligible for a second claim, in addition to the above-mentioned criterion, the treatment must also be performed on a location of stenosis or obstruction in a major coronary artery where no stenosis greater than 60% was identified in the medical examination report relating to the first claim.

8 The diagnosis relevant to the second claim must be supported with the new evidence consistent with the diagnosis of another Heart Attack or Stroke.

9 Subject to US$50,000 / HK$/MOP400,000 per type of illness per life limit under all benefits issued by the Company.

10 The amount of Total Premiums Paid is based on the “Annual Premium of Basic Plan” (excluding extra loading premiums).

11 Only applicable to the Insured aged below 76.

12 MediNet Pro is provided by Inter Partner Assistance Hong Kong Ltd. The current administration fee for each Second Medical Opinion is HK$500. For each referral to medical treatment in the USA, the current administration fee is US$500. The Insured is also responsible for paying the administration fee and for any medical treatment and other related costs in the USA. Inter Partner Assistance Hong Kong Ltd. reserves the right to review the price and the number of hospitals from time to time without prior notice. The Company reserves the right to change or cease this service at any time.

13 The maximum aggregate Sum Insured of all PrimeHealth Diabetes Care, Supplementary Cancer Benefit, PrimeHealth Saver 1000, PrimeHealth Extra Saver, PrimeHealth Benefit, PrimeHealth Extra Care, PrimeHealth Saver 100+, Critical Illness Supreme 100+ Premium Refundable Plan, Critical Illness Supreme Benefit, Critical Illness Plus 100% Premium Refundable Plan, Critical Illness Benefit, Critical Illness Extra Benefit, Critical Illness Double Benefit, Comprehensive Cancer Benefit, Total and Permanent Disability Benefit and Update Jr. Health Benefit under the same Insured with the Company is US$1,500,000 /HK$/MOP12,000,000.

14 Once insured, the premiums will not increase as the age of the Insured increases. However, the Company reserves the right to adjust the premium rate for all Insured of the same risk class.

The above content contains general information and is for reference only. Please refer to the policy document for benefit coverage and exact terms and conditions. For enquiries, please contact our consultants, franchised agents or brokers, or call our Customer Service Hotline: Hong Kong (852) 2533 5555, Macau (853) 2832 2622.